If you are concerned about the rising cost of home insurance you might want to attend and learn what the insurance companies are doing in reference to “frequency and intensity of storms” ie climate change.

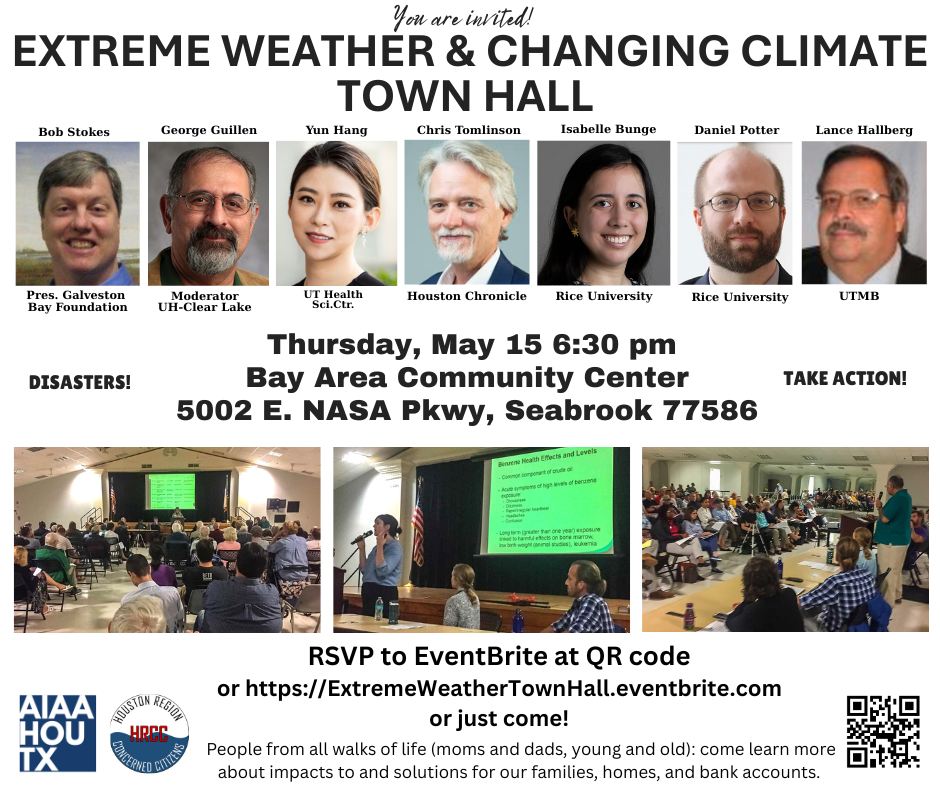

Major meeting Extreme Weather & Changing Climate next week, Thursday May 15 6:30 pm at Bay Area Community Ctr. Power panel of experts address key issues of extreme Texas weather and changing climate concerns/actions. Expertise in extreme weather, disasters and resilience, climate change, environment and human health, impacts to Gulf and bays, environmental organizations.

Galveston Bay Foundation – Bob Stokes, Director Houston Chronicle – Chris Tomlinson columnist UT Health Science Center – Dr. Yun Hang, extreme weather & natural disasters Rice U – Dr. Isabelle Bunge, climate change and human health Rice U – Dr. Daniel Potter, Houston population research UT Medical Branch – Dr. Lance Hallberg, environmental health and toxicology UH-Clear Lake – Dr. George Guillen, former director Environmental Institute, our moderator

Side Sour Note: Since my visit to Austin I have been overly busy and have neglected to keep you informed of the progress of any bills that may help us with the rising cost of insurance. I left Austin extremely disappointed in the lack of attention to our situation. Let me be blunt about where we stand. No one is coming to help us. The bills being debated are nothing but minor changes that will NOT help reduce our premiums. There are some Legislators who understand our situation and are trying but they are overwhelmed by the opposition in Austin. Where do we go from here? I do not know.

Bills being debated: Megan Kimble of the Houston Chronicle just wrote an excellent article, “Texas plan to rein in home insurers doesn’t go far enough” concerning a number of bills making their way through Austin. Take some time to read it to understand where we stand.

Our State Representative and Senator HB2067/SB1006. State Representative Dennis Paul and Senator Mayes Middleton filed HB2067 and SB1006 which are “companion” bills. Companions make it easier to fast track. Both are on their way to passing but will have no effect on our situation. The bills require an insurance company to write a letter when they cancel or deny service to you. That’s all it does. Expect them to boast about this accomplishment soon after the session is over.

Senator Mayes is stepping away from his seat to run for Texas Attorney General and Dennis Paul is rumored to be retiring. Maybe we can find two candidates who will champion our cause in 2026.

HB2741 will prohibit the use of credit scoring in setting premiums. It was left pending in the Insurance Committee in early April. SB1644 Will require an insurance company to write a letter if your credit score negatively affects your premiums. It seems ready to pass. Once again pretty useless.

SB1643 will require insurance companies to justify an increase in a rate over 10%. It passed the Senate. This bill does NOT apply to increases in premiums. It is for rate increases. Your rate may not change but your premium might double. This bill does absolutely nothing for us.

HB1576/SB2924 will create a “Fortify” program similar to Alabama. In Alabama the state helps you fortify your home from weather events in exchange for lower premiums. The Texas bill does not guarantee lower premiums. Why anyone would go through the expense of fortifying a home without an incentive is beyond me. The House bill has passed the house. The Senate bill is coming up for a hearing.

No bills were filed to address the cost of repairs or price gouging after a weather event.

Our Representative, Dennis Paul, filed HB 2067. The hearing for HB 2067 was held on Tuesday March 26 starting at 8:00 am in Austin. The bill will simply require an insurance company to write a letter to a policy holder if they deny or cancel their policy. That’s it. Nothing more. It will NOT lower our premiums or deductibles.

You can view the entire hearing here. It starts at 1:30 and runs for about 15 minutes. I spoke with every staff member responsible for the bills in the Insurance Committee and urged them to, at the very least, require the insurance companies to report this information to the Texas Department of Insurance so we can know what companies do not do business in our area. That was not discussed in the hearing. I also met with Representative Paul last week concerning this issue.

At the end of the hearing a member of the TDI touched on the lack of this data being available to the consumers but unless a bill addresses this issue nothing will be done. This bill does not address this issue.

Thank you for sending your comments to the committee. There are other bills being addressed. I will keep you informed.

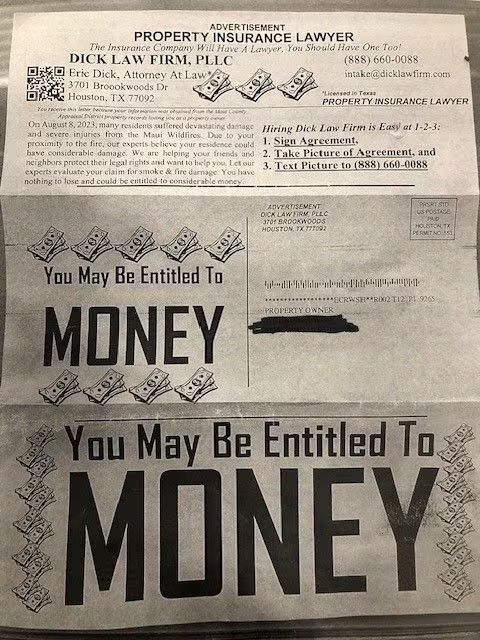

This is getting old. You have to wonder how in the living hell Harris County Department of Education Trustee, Eric Dick, is still an attorney. The Hawaiian Attorney General has filed charges against Eric Dick for Unauthorized Practice of Law after Dick solicited clients affected by the Maui fires. According to the charges:

ERIC DICK did intentionally, knowingly, or recklessly engage in or attempt to engage in or offer to engage in the practice of law, or did or attempted to do or offered to do any act constituting the practice of law, without a license or authorization so to do by an appropriate court, agency, or office or by a statute of the State of Hawaii or the United States, thereby committing the offense of Unauthorized Practice of Law in violation of Sections 605-14 and 605-17 of the Hawaii Revised Statutes.

The AG has charged him with 4 misdemeanor counts. You can read the entire document here and the back story here.

Being charged for the Unauthorized Practice of Law is just another in a series of of bad news facing Dick including:

Our Representative, Dennis Paul, filed HB 2067. The hearing for HB 2067 is scheduled for Tuesday March 26 starting at 8:00 am in Austin. The bill will simply require an insurance company to write a letter to a policy holder if they deny or cancel their policy. That’s it. Nothing more. It will NOT lower our premiums or deductibles. Contact the members of the committee and voice your concerns. (Talking points below)

Then send your comments to the following with the subject line Comments on SB1006. You can also call and and ask to talk with someone about HB2067 in the Insurance Committee. Send it to the following:

We are in dire need of premium and deductible relief.

This bill will not reduce our premiums

This bill will not make our deductibles reasonable

At the very least this bill should require the insurance companies to report denial of service to the Department of Insurance and make this information public.

And it just got worse. A home owner, Thuan Pham, has filed suit against Dick for filing a suit against an insurance company without his consent or knowledge. According to the original petition, Pham hired a roofer to repair damage to his home back in 2020. The roofer referred this claim to Eric Dick, an insurance lawyer. Pham was unaware that Dick was representing him against the insurance company. Dick eventually filed suit against the company without authorization by Pham. It gets worse.

Two years later Dick received an award from the appraisal process and deposited the check into the law firms account. The petition claims Pham’s signature was forged. Dick eventually filed a nonsuit on behalf of Pham. In 2024 Pham learned of the suit and the award and has filed suit against Dick.

This is truly some crazy shit. You can read the entire petition here.

A Report from Austin (BTW halfway through my visit I received my renewal notice. My home insurance increased from $6000 to $9000)

Last week I was joined by another homeowner from the Bay Area at the Capitol (Thanks Doug). We were able to talk with the staff of most of the members of the House Insurance Committee concerning the rising cost of home insurance in our area. The bottom line? I don’t think they understand the severity of the situation here in the Bay Area..

We were able to meet with our State Representative Dennis Paul and his Chief of Staff. As you may know Representative Paul lives two blocks from me and he had his roof replaced after the hail in May so he must know what we are going through but our conversation was not what I expected. He had a lot of excuses for the rising cost of insurance including inflation, supply chain issues, and lawsuit abuse. All of these combined could not account for excessive rates in our area. These are talking points used by the insurance industry. They also talked very briefly about “climate change” or as they call it “frequency and intensity of storms)

We made sure they were aware of the excessive cost of repairs which directly affect our premiums. Roofs replacements after a storm should not cost $32,000 in our area especially when that roof would cost only $8000 under normal conditions. (My estimate was $24,000 and was submitted as $40,000 to my insurance company)

We discussed the fact that the “Free market” is letting the insurance industry free to leave the market. The top 6 companies in Texas will NOT write policies in our area. We are now being pushed into a socialized market run by the State, the Texas Fair Plan, which is not fair.

We provided some solutions like using better building materials, automatic cutoff valves for water pipes, the use of metal roofs.

I have provided the letter we left with them below. I will have a list of bills affecting our insurance premiums early next week.

Property owners in the Bay Area are being hit with the highest premiums in the State affecting homeowners, businesses, realtors, taxpayers, home buyers and sellers, and even insurance agents. What can you do about it? For a start do this:

Join our newsletter and keep up with what is going on in Austin concerning the rising cost of insurance. We have over 850 signed up! Sign up here: tinyurl.com/BayAreaHouston. I will send a periodic email to keep you informed. No spam and I will NOT share your information with anyone.

Contact our elected officials:

Remember this is NOT a partisan issue. Everyone no matter what party you side with are affected by this issue.

State Representative Dennis Paul. He sits on the Insurance Committee. Email him and his Chief of Staff AND call his office voicing your concerns. Dennis.Paul@house.texas.gov and Greg.Bentch@house.texas.gov ((512) 463-0734)

Feel free to call me or email me. johncoby@sbcglobal.net 281-536-2457

There is no simple solution to this issue. There are no knights in shining armor that will swoop in to help. We are on our own on this issue. In the short future I will try to suggest alternatives for those looking for help.

The Business and Commerce held a hearing on Senate Bill 1006 filed by our Senator Mayes Middleton. I’ve been critical of the bill since all it will do is require an insurance company to send a letter to explain why they canceled your policy or denied you service. It does NOT require this information to be provided to the Texas Department of Insurance and made available to the public. You can view the entire meeting here starting at 1:19:30. Here is a recap:

The insurance companies are NOT in favor of this simple bill.

The insurance companies already are required to provide this information IF you ask.

Senator Zaffarini asked if this information concerning cancellations and denials are being collected by TDI. (They are not) The Houston Chronicle wrote a story on this problem.

FYI. The members of the Texas Coalition for Affordable Insurance Solutions, Allstate, Farmers, Farmers Bureau, USAA, Nationwide, and State Farm will NOT write new policies in our area.

This letter could help homeowners fight the insurance company if the reason for denial contains false information.

Our Senator Mayes Middleton filed SB1006. The hearing for SB1006 is scheduled for Tuesday March 4 starting at 10:00am in Austin. Our State Representative Dennis Paul filed a “companion” bill which is an exact duplicate. The bill will require an insurance company to write a letter to a policy holder if they deny or cancel your policy. That’s it. Nothing more. It will NOT lower our premiums or deductibles. Please send comments to the following with the subject line Comments on SB1006. Click here to email each. You can also call and and tell them you want to talk with someone about SB1006 in the Business and Commerce Committee. Send it to the following:

We are in dire need of premium and deductible relief.

This bill will not reduce our premiums

This bill will not make our deductibles reasonable

At the very least this bill should require the insurance companies to report denial of service to the Department of Insurance and make this information public.

Posted by johncoby

Posted by johncoby