Not promising for us concerned about home insurance.

State Representative Dennis Paul raised $55,905 in his latest reports covering the period of July-December 2024. That actually is one of his most productive reports. Of that total $54,600 or 98% came from PAC money and $1,304 came from 6 individual donors. Of these $8500 came from insurance related PACs. Paul sits on the House Insurance Committee.

During the same period he spent $39,049 with $22,500 going back to a number of PACs including Realtor PACs, USAA, General Contractors PAC, and BearBacker PAC. $15,000 went to pay off his outstanding $150,000 loan to win the seat over 10 years ago. He received $2500 from the BearBacker PAC then turned around and donated $2500 back to them. BearBacker PAC is related to the Baylor Bears according to their Facebook page.

If you would like to read the report on the interim charges to the Texas Senate Business and Commerce Committee it is available online here starting on page 19. It is interim charge 7 titled “Addressing the Rising Cost of Insurance. It is only 2 pages. Here are my notes/thoughts.

The Committee held a hearing on Oct 1. The testimony was dominated by the industry.

Texas has the 2nd largest market in the nation bringing in $290 Billion in premiums.

The increase in premiums are due to climate change, inflation, labor expenses, supply chain disruptions and reinsurance (LOL. They are using climate change against us to increase our premiums. Inflation is well under control and has been for a while but it did NOT account for a doubling of premiums. Supply chain disruptions were corrected years ago.)

They ignored the inflated cost of roofing after an event such as hail or extreme weather. Why does a roof cost $24,000 to replace after an event, but only $6000 at other times?

They blame us for not “shopping around”.

TDI stated only 4 companies left Texas in 2024 but ignored comments from area such as the Bay Area where 5 of 6 members of the Texas Coalition for Affordable Insurance Solutions (TCAIS) will not longer write policies.

There was a significant uptick in the Texas Fair Access to Insurance Requirements (FAIR) Plan from 72,626 to 91,841 from 2003 to 2024.

TDI claims homeowners in Texas saw an average rate increase of 21% in 2023. I’m not sure if that is a rise in rates or premiums which are two different things.

TDI reviewed 1313 rate filings with 107 filings withdrawn, 78 rejected for administrative discrepancies. They did not disclose how many rate increases were rejected by TDI.

The recommendations are basic if not ridiculous.

Implement guardrails to protect against unfair pricing practices, which could include, but is not limited to, rate filings and premiums assessed to policyholders.

Support the efforts of both TDI and OPIC to improve notice to policyholders about rate changes, coverage reductions, and comparison-shopping tools.

I have secured the Webster Activity Center on Jan 7, 2025 for another community meeting to discuss and take action concerning the rising cost of home insurance in our area. We will focus on the upcoming legislative session and how we can take the opportunity to influence our elected officials. For those who are not aware this session begins Jan 14 and will continue till June 2.

Our elected officials have been invited to attend and discuss what we can do. Please save the date, invite your neighbors, and I will see you Tuesday. Preliminary agenda:

And you wonder why your insurance premiums are so high?

I filed a claim for roof damage after Hurricane Ike in 2008. I received about $5000 from USAA, my insurance company at the time. Bids for the roof replacement ranged from $10,000-$16,000. At the time I did not have the extra funds to pay for the roof and since there was no leaks I put the repairs off for 2 years.

In 2010 I had my roof replaced for $4800. One of the companies that quoted over $10,000 in 2008 provided a quote of $6800 in 2010. At the time I knew the Commissioner of the Texas Department of Insurance and mentioned the price gouging after a hearing in Austin. Soon afterward he left the Commission and I ended my consumer activism.

So here we are in 2024 and I filed a claim for hail damage. Eventually I had my roof replaced for a cost that was listed at $24,000 about 5 times what I paid in 2010 just 14 years ago. I’ve heard from others in my subdivision whose estimates were even higher, $32,000 for one homeowner. What is disturbing is that the insurance companies are paying these inflated prices. It’s a win-win for the roofer and the insurance company who can simply pass the inflated cost to consumers in higher premiums. Everyone is happy except for the consumer.

Last year Harris County Attorney filed a number of suits resulting in settlements for price gouging of gasoline. According to Houston Public Media:

The Bellaire location allegedly sold regular unleaded gasoline for $3.79 and $4.29 per gallon, an increase of 25% and 41% respectively from the gas station’s pre-hurricane price of $3.03. The Baytown location was allegedly selling premium gasoline for $5.49 per gallon, which is 44% higher than the gas station’s pre-hurricane price of $3.80.

Price gouging after an event like a hurricane is illegal. Raising the cost of a gallon of gas by 40 cents can be considered price gouging and could be investigated by the County Attorney. Charging 2 to 4 times the regular price for a roof should be considered price gouging.

Sixteen years ago States along the coast began implementing a plan called Fortified, including Alabama. According to an article written by Megan Kimble of the Houston Chronicle: “Alabama offers $10,000 grants to homeowners to upgrade their roofs – and requires insurers to give discounts of 25% to 55% to those who do”. That program started 16 years ago!! What the hell did elected officials in Texas do?

Nothing. Not a goddamn thing and now we are paying for it. Literally. We are now in crisis mode with premiums out the roof, excessive deductibles, and companies threatening to leave the Sate. In the upcoming legislative session bills will be filed to protect the insurance industry at our expense. While other States were actively working to lower the risk our elected officials did nothing to protect our homes. This article is another in her series concerning home insurance. It’s a VERY good read. I should be available to read here. It might make you mad. Let me summarize:

While other states on the coast, like Alabama, took action 15 years ago to reduce the risk to homeowners, Texas did nothing, at all, except pass the cost of the risk to consumers.

Other states give incentives to homeowners to “fortify” their homes and requires reduced insurance premiums.

A bill has been filed in Texas to create a program similar to Alabama’s “Fortified” but does NOT require a reduction in premiums

Of the country’s 70,000 Fortified homes, only 200 are in Texas and half of those were built by Habitat for Humanity.

While Texas officials were busy cutting regulations and chasing social issues we were left to find our own insurance solutions.

I love this quote “Home builders along the coast say they already follow stringent building standards and don’t need more.”

“In coastal Alabama and North Carolina – both states that incentivize Fortified standards – researchers say homes certified through the program have shown a 20% reduction in losses compared to non-Fortified homes.”

Alabama offers $10,000 grants to homeowners to upgrade their roofs – and requires insurers to give discounts of 25% to 55% to those who do. That program started 16 years ago!!

So take some time to read the article then make plans to attend our next meeting.

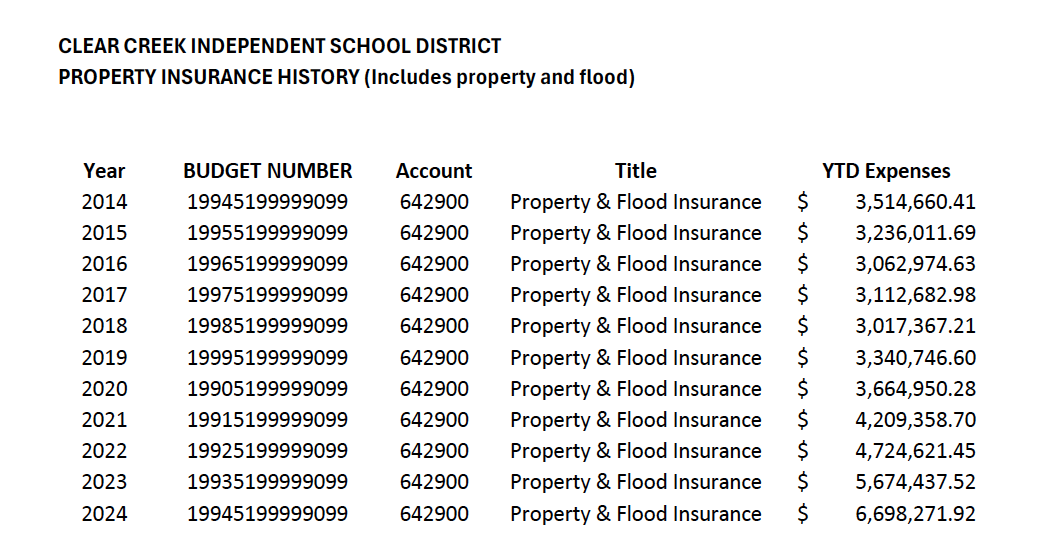

As said before the rising cost of property insurance is affecting everyone in the Bay Area, including taxpayers. According to an open records request CCISD’s property insurance doubled in just five years from 2019-2024. In 2019 CCISD’s property and flood was $3.3M. In 2024 it was $6.6M. This is not solely due to inflation. There is much more to this increase than inflation.

Everyone is paying for the rising cost of insurance including homeowners, businesses, government entities and taxpayers. Come join us next year to have a discussion with elected officials.

In 1971 Texas created the Texas Windstorm Insurance Association (TWIA). It was advertised as the insurance of last resort covering those in the coastal areas who could not find insurance from the private sector. In 1995 Texas created the Texas Fair Plan Association (TFPA). It was advertised as the insurance of last resort covering those in the under served areas who could not find insurance from the private sector. Sound familiar?

Up until 2003 TWIA was providing service to a small number of property owners. Now it isn’t the last resort. It’s almost the only resort. Private insurance companies have fled the coastal areas leaving most owners to seek coverage from TWIA. I have little knowledge of TWIA, except that they are a non-profit organization and sell policies just like the private sector. TWIA issues detailed yearly assessments of their policies and financial situation. They are transparent to the public. When they ask for a 10% increase in rates they can prove it with data, data that is publicly available.

When did you ever see your insurance company justify their 25% increase or the reason why they will not renew your policy? As with TWIA I know little about the Texas Fair Plan except that they are managed by TWIA and like TWIA they are the insurance of last resort. They are also transparent and a non-profit. I think homeowners in the Clear Lake area should read the articles about the TFPA because it may become the last resort. 5 of the 6 largest insurance companies in Texas that make up the Texans for Affordable Insurance Solutions (TCAIS) will no longer write policies in the Clear Lake area.

Maybe it is time for all insurance companies to leave the state and let the non-profits provide service.

The articles by Houston Chronicle reporter, Megan Kimble, concerning the rising cost of home insurance are lengthy yet highly informative reads. If you can access the articles, take some time to read them. Here are my thoughts on the article:

Elected officials are not immune from increases. Senator Tan Parker out of the Dallas area says he was dropped by his company and is now paying three times as much for his insurance. State Rep. John Smithee, an Amarillo Republican had his premiums raised by 40% last year. He authored the insurance bills of 2003. Our own State Representative had his roof replaced last month. I am sure he has felt the pinch.

Our elected officials are missing in action. Where are our State officials? Our Representative, Dennis Paul, sits on the Insurance Committee. Where has he been? In office for 10 years he has NEVER convened a town hall meeting to address the issues of the community. We are now in crisis mode and he has still refused to respond to his constituents except for form letter responses if even that. The same can be said about our State Senator Mayes Middleton. Both have been asked to address the community at our Jan 7th meeting.

Climate Change. For decades the industry and elected officials have denied climate change but are now claiming that is the main factor in the rising cost of insurance. So they did nothing over the last 20 years to minimize the risk due to climate change and are now passing the consequences on to us.

Rates vs Premiums. This wasn’t specifically discussed in the articles but realize rates and the cost to rebuild determines your premium. So when the Texas Department of Insurance says that rates only went up by 21% over the last few years that might be true but the cost to rebuild has skyrocketed as has your premiums. Case in point USAA based the cost to rebuild my home at $645,000 driving my premium up over $15,000. Your deductible is also based upon a percentage of the cost to rebuild.

The Texas Coalition for Affordable Insurance Solutions. They are quoted in the article. They are a lobbyist group funded by the top 6 insurance companies in Texas. Over the last 20 years they have done NOTHING to find solutions for affordability. I have written about them here. The same lobbyist quoted in the article was the same one leading the fight to reform insurance back in 2023.

Lowering the risk and damage. Other states have been proactive in addressing the issue by encouraging better storm resistant products for homes and roofs. They have created incentives for homeowners to use these products. Texas has done nothing over the last 20 years. Even our HOAs can refused the use of these products and the State will do nothing to stop them from enforcing it. There are hail resistant roofs available, even metal ones, and water cut off valves that could detect a leak and prevent damages to a home due to busted pipes. The industry along with our elected officials are finally discussing these possible solutions, 20 years too late. There have been fills filed to address this issue but the Republic Party in the Senate killed them.

Inflation. Yes some of the increases can be attributed to inflation but it is NOT responsible for a 50% increase or a 100% increase. This, along with climate change, are a great excuses to justify dropping your coverage or over charging. Inflation is now under 3%.

Surge Pricing. This wasn’t discussed in the articles but it is real. Why does a roof cost $30,000 when it usually would cost just $8,000? In 2008 after hurricane Ike bids for a new roof ranged from $10,000-$15,000. I had my roof replace two years later for $4800. This year after a hail storm bids were coming in at $23,000 for the cheapest roof. My roofer eventually quoted $24,000. This needs to be addressed.

I have secured the Webster Activity Center on Jan 7, 2025 for another community meeting to discuss and take action concerning the rising cost of home insurance in our area. We will focus on the upcoming legislative session and how we can take the opportunity to influence our elected officials. For those who are not aware this session begins Jan 14 and will continue til June 2.

Our elected officials have been invited to attend and discuss what we can do. Please save the date, invite your neighbors, and I will see you after the holidays.

Spread the word

Thank you for staying engaged. As of today we have almost 700 individuals who have signed up for for our newsletter. I am now expanding this activity to statewide. Please spread the word and invite your friends to join this list at tinyurl.com/BayAreaHouston. Also you can post this information on your social media platforms including Facebook and Nextdoor.

If there is a guide on “How to lobby elected officials” I have not found it. So I will give you an idea of what we could do just based upon my experience as a consumer activist years ago. I don’t expect to know it all so if you have ideas, I am all ears.

Be focused. Stay on message. For the insurance issue the message should be very clear: We want our premiums to be lowered, our deductibles to return to a fixed amount not more than $1000, and we do NOT want a deduction in coverage.

Develop a relationship to your elected official or their staff. Call your elected official in Austin and ask for the staff member assigned to insurance issues. Ask for an email address. Then keep in touch. Make sure you send them any information you think is important to the issue. For our area contact Greg Bentch at greg.bentch@house.texas.gov with State Representative Dennis Paul and Matt Patterson at matt.patterson@senate.texas.gov with Senator Mayes Middleton’s office.

Contact the members of the specific committee that will hear the bill(s) you are concerned about. The insurance bills in the House will most probably be assigned to the State Affairs Committee. The Chair lives in the Corpus Christi area and has an interest in this issue. I have collected the contact information for the members. I have listed them below. Again, contact each one with your specific information. If you can, call and email them.

Visit your elected officials office. Make an appointment in the district. Talk with someone about your insurance issue. Dennis Paul’s office is at 17225 El Camino Real Blvd Suite 415 (281) 488-8900. Senator Middleton’s office is at 174 Calder Road Suite 900 League City, TX 77573 (281) 332-1000

Spend a day in Austin. What I have done in the past was to make appointments with the staff members of the elected officials on the committee. The State Affairs Committee has 13 members. If you spend 15 minutes with each you might talk to all of them in 1 full day. That is a tough day. When you visit make sure you have a written copy of what you intend to talk about. Keep it to the point. Make sure they hear and understand our message.

Attend a hearing. This will be covered in a later email.

So. You can start now. Here are some important contacts:

State Representative Dennis Paul Insurance Committee C/O Greg Bench greg.bentch@house.texas.gov (512) 463-0734 Austin phone 17225 El Camino Real Blvd Suite 415 (281) 488-8900.

Senator Mayes Middleton Business and Commerce Committee C/O Matt Patterson (512) 463-0111 Austin Phone 174 Calder Road Suite 900 League City, TX 77573 (281) 332-1000

You can find the contact info for members of the State Affairs Committee here. They will be hearing the bills.

I am working on the Business and Commerce Committee.

Posted by johncoby

Posted by johncoby